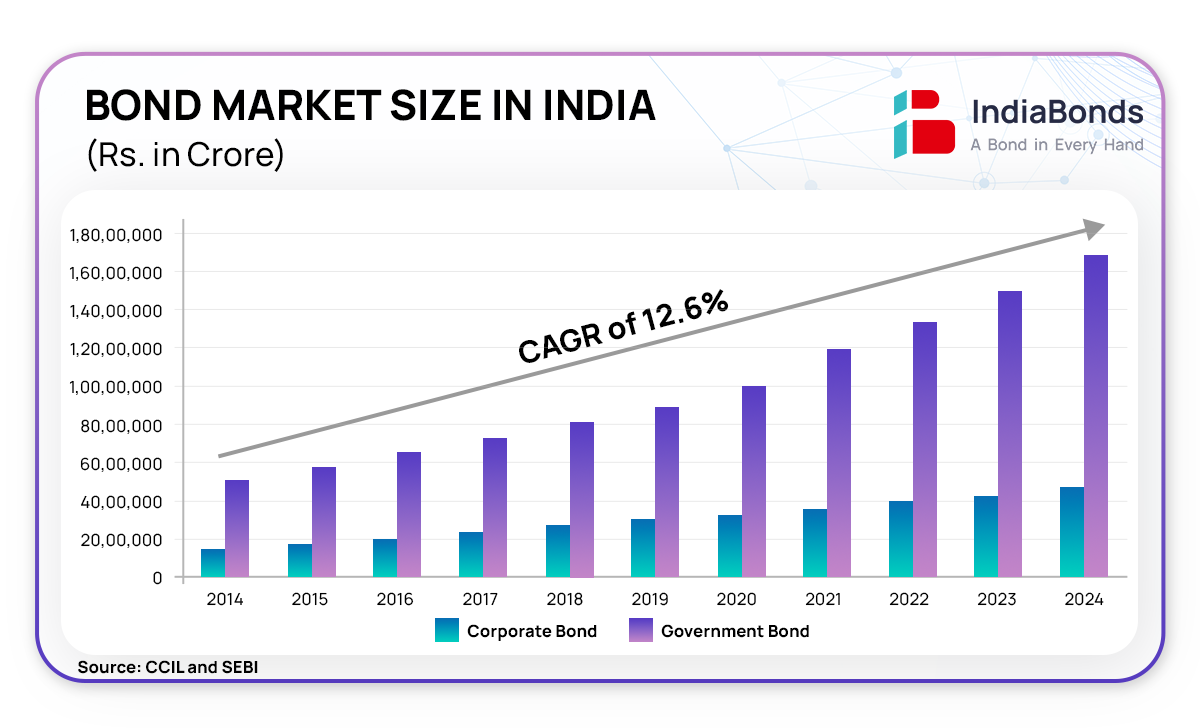

Size of the Indian Bond Market is US$ 2.64 trillion!

5.67K

5.67K

Introduction

The Indian bond market is a critical component of the nation’s financial ecosystem. This substantial market size not only highlights the maturity and depth of India’s debt instruments but also underscores the potential for future growth. In the context of global financial landscapes, where the world’s bond market stands at a staggering US$133 trillion, India’s bond market emerges as a significant player with immense opportunities for expansion. This article explores the current state and future prospects of the Indian bond market, providing insights into its structure, growth trajectory and the pivotal role it plays in funding the nation’s economic aspirations.

Global Sizing

As of 2023, the world’s GDP was estimated to be around US$101 trillion (Source: World Bank), the world equity market cap stood at US$106 trillion and the global bond market at US$133 trillion (Source: SIFMA). The stats for the largest economy in the world are even more interesting. The US GDP in 2023 was estimated to be US$26 trillion. Its equity market cap was at US$45 trillion, but its bond market was a whopping US$53 trillion! (Source: SIFMA). These numbers have seen significant growth post-2020 due to the massive stimulus and liquidity injection by the US following the Covid-19 pandemic. The All India equity market capitalization stood at almost US$4.98 trillion (Source: BSE). As you already know, the Indian bond market now stands at about US$2.59 trillion (Source: CCIL and SEBI). It is striking to observe that although the bond market in India is large, it has a significant scope for explosive growth from here.

Market Structure

The bond markets in India have matured significantly in the last ten years, providing a relatively safe investment avenue for investors. The broad segments of the market are Central Government Securities (G-Sec), State Development Loans (SDL) and Corporate Bonds. Market depth in these securities has experienced consistent growth in terms of primary issuance as well as growing trading volumes in the secondary market.

RBI regulates G-secs, SDLs and money markets, while SEBI regulates the corporate bond market. If you were not already aware, you will be surprised to know that almost everyone is indirectly an investor in the bond markets. This is because the largest institutional investors in bond markets are all the insurance companies, pension funds and mutual funds. Apart from the domestic institutions, other significant investments come from FPIs (Foreign Portfolio Investors). Another aspect that is gradually growing is the retail and individual investment participation, specifically in the corporate bond market.

The Indian Context

The outstanding bond market in India is valued at US$2.59 trillion (Source: CCIL and SEBI), showing an annual growth of 12.3% in INR terms from the previous year. The corporate bond market, valued at US$567 billion, also grew by 12.6% year-over-year. Structurally, the debt market remains skewed towards government securities (G-secs). To put this into perspective, the outstanding government securities stock is Rs. 1,68,85,262 crores (US$2.02 trillion), while the outstanding corporate bonds are Rs. 47,28,935 crores (US$567 billion) (Source: CCIL and SEBI).

The entire bond market in India has grown at an impressive annual rate of 12.6% in INR terms in the past decade. This growth is indicative of the expanding role of bond markets in India’s financial ecosystem. Moreover, the inclusion of Indian bonds in global indices by JP Morgan and Bloomberg has put Indian fixed income on the global map.

SEBI Amendments for Corporate Bonds

SEBI has recently proposed pivotal changes to the corporate bond market, significantly reducing the minimum investment size from INR 1 lakh to just INR 10,000. This phased reduction—from ₹10 lakh to ₹1 lakh and now to ₹10,000—aims to increase participation while maintaining safety. Additionally, SEBI has introduced two key changes to enhance market efficiency: standardizing record dates for bond interest payments and redemptions to 15 days before the due date, streamlining operations and clarifying payment timings for investors and enhancing the dissemination of financial information through technologies like weblinks and QR codes, reducing paper reliance and ensuring swift access to vital details. The creation of Online Bond Platform Providers (OBPPs) and tighter regulations on unlisted bonds further demonstrate SEBI’s commitment to expanding the market while safeguarding investor interests. We are standing at the cusp of a bond revolution in India, and the factors stated above are only going to poise the market for unprecedented growth and participation.

Outlook for the Future

S&P Global Ratings has revised India’s credit rating outlook from ‘stable’ to ‘positive,’ highlighting policy consistency, significant economic reforms and substantial infrastructure investments as key factors driving sustained long-term growth. The projected growth of India’s GDP to US$5 trillion in the next few years is going to be funded largely by credit provided to corporations through the bond markets. We have already witnessed this in the western economies where the corporate bond market is a large percentage of GDP (up to 50-65% in some cases). As India transitions from a developing to a developed economy, the sophistication and depth of its financial markets hold the key to economic upliftment. Households that transfer their huge savings to investments and in this case to a safer asset class of corporate bonds, will likely spur exponential growth of corporate bonds and provide the funding for India’s credit story. It is our effort at IndiaBonds to be a catalyst for this growth and make bond investments easy for individuals. Currently, bond markets are big – however, they are only going to get bigger! Don’t get left behind…

Disclaimer: Investments in debt securities/ municipal debt securities/ securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully.

5.67K

CIN: U67100MH2008PTC178990 |

SEBI Registration No.: INZ000311637 |

NSE Member ID - Debt Segment: 90316 |

BSE Member ID - Debt Segment: 6811